If they send one to eight participants, the fixed cost for the van would be \(\$200\). If they send nine to sixteen students, the fixed cost would be \(\$400\) because they will need two vans. We would consider the relevant range to be between one and eight passengers, and the fixed cost in this range would be \(\$200\). If they exceed the initial relevant range, the fixed costs would increase to \(\$400\) for nine to sixteen passengers. The contribution margin shows how much additional revenue is generated by making each additional unit of a product after the company has reached the breakeven point. In other words, it measures how much money each additional sale “contributes” to the company’s total profits.

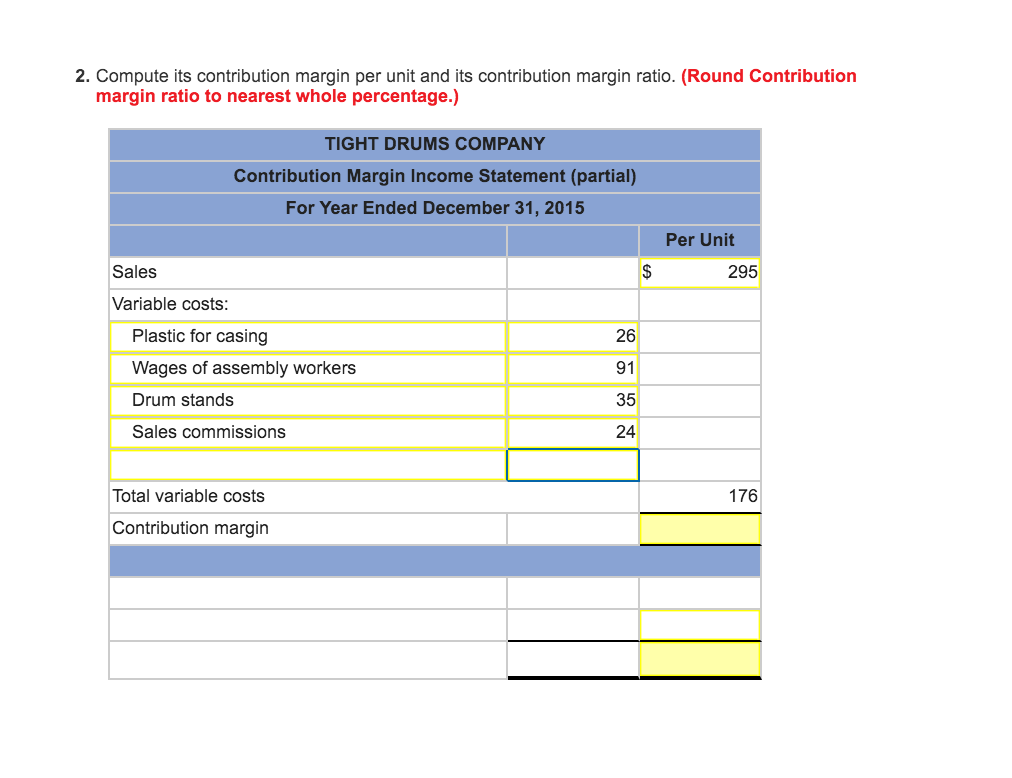

Example of how to find the contribution margin

Fixed expenses will increase if there is a step cost situation, where a block of expenses must be incurred to meet the requirements of an increase in activity levels. For example, sales may increase so much that an additional production facility must be opened, which will call for the incurrence of additional fixed costs. A contribution income statement is an income statement that separates the variable expenses and fixed costs of running a business.

- Accountants can make an allocation on the basisof benefit received for certain indirect expenses.

- A high contribution margin indicates that a company tends to bring in more money than it spends.

- The concept of contribution margin is applicable at various levels of manufacturing, business segments, and products.

- For the month of April, sales from the Blue Jay Model contributed \(\$36,000\) toward fixed costs.

- A cost objectis a segment, product, or other item for which costs may beaccumulated.

Activity Sampling (Work Sampling): Unveiling Insights into Work Efficiency

To demonstrate this principle, let’s consider the costs and revenues of Hicks Manufacturing, a small company that manufactures and sells birdbaths to specialty retailers. For example, assume that the students are going to lease vans from their university’s motor pool to drive to their conference. A university van will hold eight passengers, at a cost of \(\$200\) per van.

Concepts used in segmental analysis

You will also learn how to plan for changes in selling price or costs, whether a single product, multiple products, or services are involved. The “total income before tax” line on the contribution format income statement is the difference between the contribution margin and fixed costs. Fixed costs are costs that do not change relative to the amount of production. Rent, utilities, payroll and other administrative expenses not related to sales or production are considered fixed costs.

If we subtract the variable costs from the revenue, we’re left with a $22,000 contribution margin. COGS only considers direct materials and labor that go into the finished product, whereas contribution margin also considers indirect costs. For instance, Nike has hundreds of different shoe designs, all with different contribution margins. Putting these into a traditional income statement illustrates the bigger picture of which lines are doing better than others, or if any shoes need to be discontinued. Watch this video from Investopedia reviewing the concept of contribution margin to learn more. Keep in mind that contribution margin per sale first contributes to meeting fixed costs and then to profit.

Before starting his writing career, Gerald was a web programmer and database developer for 12 years. My Accounting Course is a world-class educational resource developed by experts to simplify accounting, finance, & investment analysis topics, so students and professionals can learn and propel their careers.

Another common example of a fixed cost is the rent paid for a business space. A store owner will pay a fixed monthly cost for the store space regardless of how many goods are sold. Investors and analysts use the contribution margin to evaluate how efficient the company is at making profits. For example, analysts can calculate the margin per unit sold and use forecast estimates for the upcoming year to calculate the forecasted profit of the company.

When preparing internal reports on theperformance of segments of a company, management often finds it isimportant to classify expenses as fixed or variable and as director indirect to the segment. As a result, many companies prepare an income statementfor internal use with the format shown below. The contribution margin is different from the gross profit margin, the difference between sales revenue and the cost of goods accounting software: email settings in xero sold. While contribution margins only count the variable costs, the gross profit margin includes all of the costs that a company incurs in order to make sales. Traditional statements calculate gross profit margin, which is determined by subtracting the cost of goods sold (COGS) from revenue. Contribution format statements produce a contribution margin, which is the result of subtracting variable costs from revenue.

In contrast, indirect costs become segmentcosts only through allocation; therefore, most indirect costs arenoncontrollable by the segment manager. Be careful, however, not toequate direct costs with controllable costs. For example, thesalary of a segment manager may be direct to that segment and yetis noncontrollable by that manager because managers cannot specifytheir own salaries. You’ll notice that the above statement doesn’t include the contribution margin. That’s because a contribution margin statement is generally done separately from the overall company income statement.

For those organizations that are still labor-intensive, the labor costs tend to be variable costs, since at higher levels of activity there will be a demand for more labor usage. To illustrate how this form of income statement can be used, contribution margin income statements for Hicks Manufacturing are shown for the months of April and May. The contribution margin represents the revenue that a company gains by selling each additional unit of a product or good.

Tyler O’Brien including said he felt the newest inform you try rigged

Tyler O’Brien including said he felt the newest inform you try rigged

Leave a Comment... Discuss!