This means that the contribution margin income statement is sorted based on the variability of the underlying cost information, rather than by the functional areas or expense categories found in a normal income statement. Traditional income statements are used to evaluate the overall profitability of a business. Contribution formats are more detailed, and are useful for evaluating business segments, such as subsidiaries or divisions, or individual product lines. They’re also useful for managers determining how sensitive variable costs are to a change in sales or production.

What is a contribution margin income statement?

Unlike the traditional income statement that categorizes costs as either cost of goods sold or operating expenses, the contribution format statement focuses on identifying costs that vary directly with sales levels. This helps in calculating the “contribution margin,” which is the revenue remaining after variable costs that can contribute to fixed costs and profit. To stress the importance of a segment’scontribution to indirect expenses, many companies prefer thecontribution margin income statement format. Notice how theindirect fixed costs are not allocated to individual segments.Indirect fixed expenses appear only in the total column for thecomputation of net income for the entire company.

The Difference Between Contribution Margin and Gross Margin

This standard format can give you a great financial snapshot of how your business is doing. But if you’d like to dig deeper and shed light on how costs affect your profit, a contribution format income statement can help. In this example, the Contribution Margin ($45,000) is the amount available to cover the fixed costs and to contribute to the net income. The Net Income is found by subtracting the total fixed costs from the contribution margin. Now you know all about the contribution margin income statement, how it differs from the traditional income statement, and how to make one.

Contribution margin vs. EBIT and EBITDA

This guide will break down what a contribution income statement is, its components, and how it differs from a traditional income statement, with examples to enhance understanding. Variable costs probably include cost of sales (the cost of goods sold) and a portion of selling and general and administrative costs (e.g., the cost of hourly labor). Retail companies like Lowe’s tend to have higher variable costs than manufacturing companies like General Motors and Boeing. Using a hypothetical company, let’s look at how a contribution margin income statement compares to a traditional income statement. These costs don’t fluctuate with the level of production or sales an item makes—which is why they’re sometimes called fixed production costs.

Example 1 – single product:

Therefore, this income statement will be based off the sale of 8,000 units. Investors and analysts may also attempt to calculate the contribution margin figure for a company’s blockbuster products. For instance, a beverage company may have 15 different products but the bulk of its profits may come from one specific beverage. The contribution margin can help company management select what is cash flow and why is it important for businesses from among several possible products that compete to use the same set of manufacturing resources. Say that a company has a pen-manufacturing machine that is capable of producing both ink pens and ball-point pens, and management must make a choice to produce only one of them. A low margin typically means that the company, product line, or department isn’t that profitable.

How Do You Calculate Contribution Margin?

- Allocating expenses based on sales is not recommendedbecause it reduces the incentive of a segment manager to increasesales because this would result in more indirect expenses beingallocated to that segment.

- Contribution formats are more detailed, and are useful for evaluating business segments, such as subsidiaries or divisions, or individual product lines.

- Since machine and software costs are often depreciated or amortized, these costs tend to be the same or fixed, no matter the level of activity within a given relevant range.

Variable cost includes direct material, direct labor, variable overheads, and fixed overheads. It does not matter if your expenses are production or selling and administrative expenses. The same thing goes with fixed expenses; they must be included in fixed costs if they are fixed.

A contribution margin income statement varies from a normal income statement in three ways. First, fixed production costs are aggregated lower in the income statement, after the contribution margin. Second, variable selling and administrative expenses are grouped with variable production costs, so that they are part of the calculation of the contribution margin. And finally, the gross margin is replaced in the statement by the contribution margin.

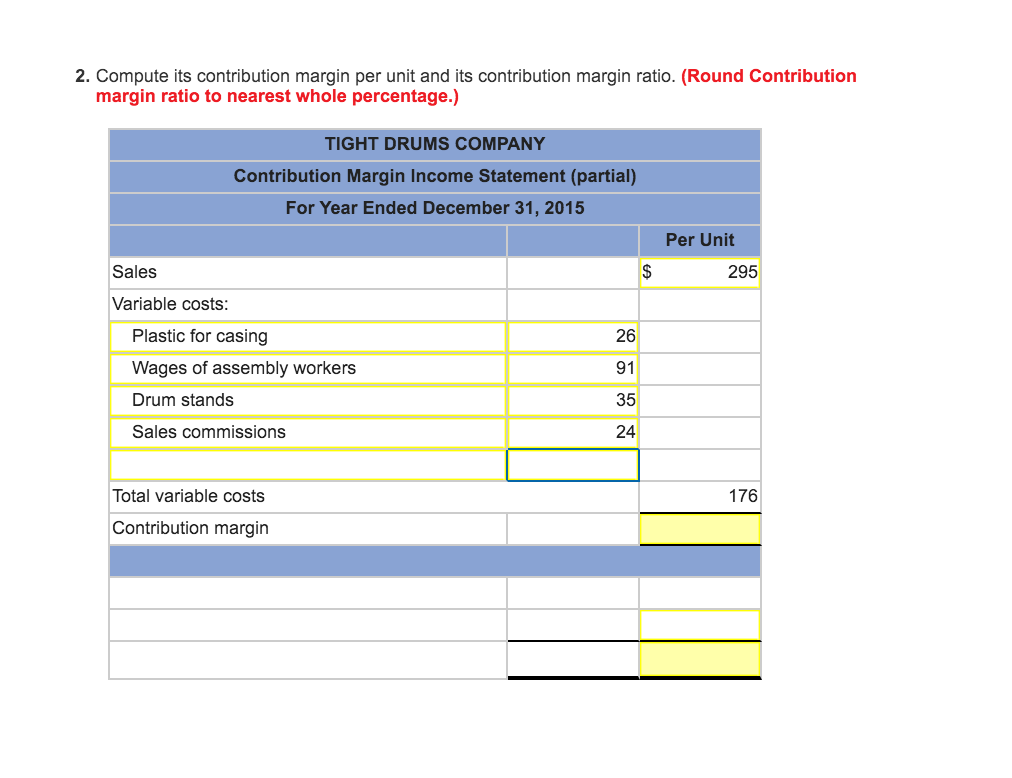

The contribution margin income statement shows fixed and variable components of cost information. This statement provides a clearer picture of which costs change and which costs remain the same with changes in levels of activity. At a contribution margin ratio of \(80\%\), approximately \(\$0.80\) of each sales dollar generated by the sale of a Blue Jay Model is available to cover fixed expenses and contribute to profit. The contribution margin ratio for the birdbath implies that, for every \(\$1\) generated by the sale of a Blue Jay Model, they have \(\$0.80\) that contributes to fixed costs and profit. Thus, \(20\%\) of each sales dollar represents the variable cost of the item and \(80\%\) of the sales dollar is margin. Just as each product or service has its own contribution margin on a per unit basis, each has a unique contribution margin ratio.

The computationfor each segment stops with the segment’s contribution to indirectexpenses; this is the appropriate figure to use for evaluating theearnings performance of a segment. Only for the company as a wholeis net income (revenues minus all expenses) computed; this is, ofcourse, the appropriate figure to use for evaluating the company asa whole. Fixed costs include all fixed costs, whether they are product costs (overhead) or period costs (selling and administrative). One thing that causes the contribution margin income statement and variable costing to differ from the traditional income statement and absorption costing is the fact that fixed overhead is treated as if it were a period cost. Therefore if there are units that are not sold, a portion of the fixed overhead ends up in inventory. The “contribution margin” is the difference between total sales and variable costs.

The best ways to make money online betting

The best ways to make money online betting

Leave a Comment... Discuss!